Follow us

Truckload capacity is tightening heading into the back half of 2026. Carriers have left the market, the driver workforce is aging, and tighter licensing rules are shrinking the pool, so fewer trucks are competing for freight and rates are firming. You don't have to settle the "driver shortage" debate to see it. The shippers who stay covered are the ones with broad, vetted carrier networks and real-time market visibility.

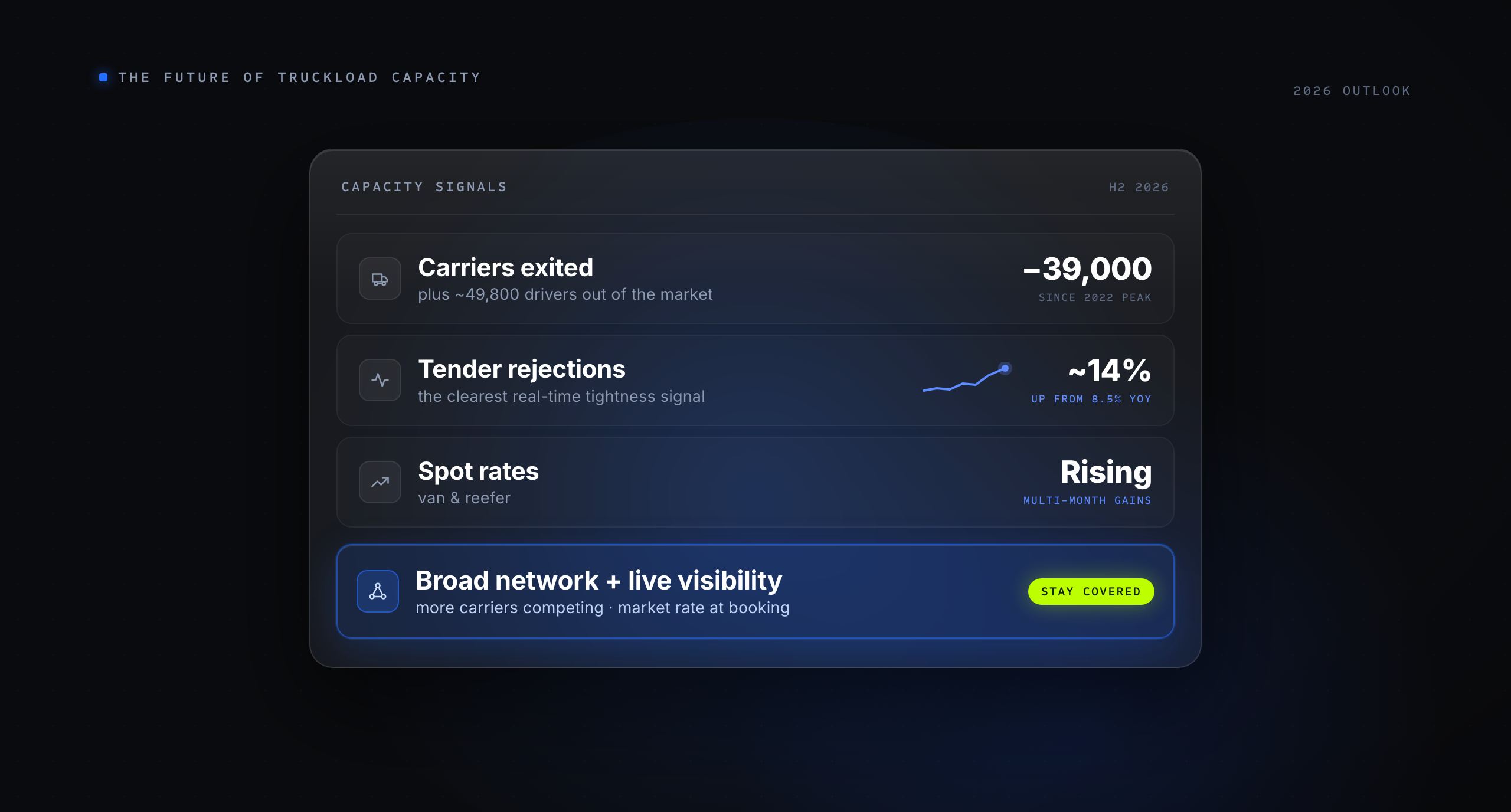

If you move truckload freight, you've probably felt it: covering loads is getting a little harder, and rates aren't drifting down the way they did a couple of years ago. Something is tightening.

You've also probably heard it blamed on a "driver shortage." That label is genuinely contested. The American Trucking Associations projects the industry could be short roughly 160,000 drivers by 2028 if current trends hold, concentrated in over-the-road truckload. Others, including a National Academies study, argue the persistent shortage has been overstated, and even the ATA now frames much of it as a quality and retention problem rather than a raw headcount gap.

Here's the good news: as a shipper, you don't need to settle that argument. The debate is about labels. What matters to you is capacity, whether there's a truck for your load and what it costs, and on that question the signals are a lot less ambiguous. So let's set the label aside and look at what's actually happening to the trucks you need.

Yes, and you can see it in the numbers that don't depend on the shortage debate.

More than 39,000 interstate carriers and roughly 49,800 drivers have exited the market from their 2022 highs. That capacity left, whatever you call the cause. At the same time, the clearest real-time signal of tightening, the rate at which carriers reject loads they're contracted to haul, has climbed sharply: the outbound tender rejection index sits around 14% in early 2026, up from about 8.5% a year earlier. When carriers reject more tenders, it means they have better options, which is exactly what happens when trucks get scarce relative to freight.

Rates have followed. Spot van and reefer rates have posted several straight months of gains, and forecasters broadly expect a firmer market through the back half of 2026 rather than a return to the soft rates of 2024. We covered the mechanics of that shift in why tender rejections are rising.

Several forces are pushing the same direction at once.

An aging workforce. A large share of the driver population is within a decade of retirement, and replacements aren't entering fast enough to keep pace. That's a slow, structural squeeze that doesn't reverse quickly.

Carriers leaving the market. The soft rate environment of the last couple of years pushed tens of thousands of small carriers out. Since most carriers run fewer than ten trucks, that exit thins capacity in a way that's hard to rebuild overnight.

Tighter licensing and enforcement. Regulatory changes in 2026, including stricter CDL standards and enforcement, have pulled additional drivers out of the eligible pool, with some states reporting sharp drops in CDL renewals.

Uneven geography. The squeeze isn't uniform. Regions like the Southeast and Texas are seeing the sharpest constraints, so a shipper on those lanes can feel a tight market long before the national averages say so.

Not on a timeline that helps you plan next year's freight.

Two technologies get pitched as the answer whenever capacity tightens: electric trucks and driverless ones. Both are real. Neither changes your capacity math in the near term.

Take the Tesla Semi, the most visible electric truck on the market. It's a battery-electric Class 8 tractor Tesla positions as "the future of trucking," with an estimated 500-mile range on the long-range version and a pitch built around lower cost per mile and lower maintenance than diesel, with volume deliveries slated to begin in 2026. What it's trying to solve is the operating cost and emissions of trucking, not the number of trucks or drivers available. An electric truck still needs a driver, and it's most viable today on regional and drayage lanes near charging, not the long-haul routes where capacity is tightest. Useful over time, not a lever you pull to cover loads this quarter.

Driverless trucks aim at the labor side more directly, and the technology is advancing. But as of mid-2026, driver-out operations number in the dozens of trucks across a few specific corridors, against roughly 4 million Class 8 trucks on the road. Even optimistic forecasts put commercial autonomy at a single-digit percentage of long-haul lanes by the early 2030s. It's a long-term shift worth watching, not something that covers your freight when a lane goes tight next month.

So the practical takeaway is the opposite of "wait for technology to fix it." The shippers who stay covered are the ones who adapt how they buy.

You can't add drivers to the market. You can control how much capacity competes for your freight and how quickly you see the market move. Four moves matter.

Widen your carrier network. The single biggest predictor of getting covered in a tight market is how many quality carriers can see your freight. A shipper relying on three or four carriers is exposed the moment one of them tightens; a shipper tapping a deep, vetted network keeps competition on the load even when capacity is scarce. This is the core of building carrier relationships that weather any market.

Make your freight easy to haul. In a tight market, carriers get selective. Fast load and unload times, flexible scheduling, and consistent volume make your loads the ones carriers want, which protects both coverage and rate.

Get the spot and contract mix right, and revisit it often. Locking contract capacity on your steady lanes protects you when rates climb, while spot keeps you flexible everywhere else. In a firming market the balance matters more than usual, and the shippers who win rebalance more than once a year. We broke this down in spot vs. contract freight.

See the market in real time. You can't react to a tightening lane you can't see. Knowing the market rate at the moment you book tells you when a lane is moving and whether a quote is competitive, so you're adjusting with the market instead of finding out after the fact.

None of these require predicting the market. They build the resilience that keeps you covered whichever way it turns.

Resilience in a tight market comes from network depth and visibility, and it shows up in performance.

Shippers who moved from a handful of carriers to a broad, vetted network consistently expand their coverage and their leverage. In a study of shippers using Dynamic Book It Now, which books spot loads against a live market benchmark across a large carrier network, 85% secured rates below market. That's what competition on every load looks like, and it's exactly the buffer that matters most when capacity tightens.

The platforms that help here are the ones that combine a deep carrier network, spot and contract in one place, and market-rate visibility, so you can adapt as conditions move rather than scrambling when a lane goes tight.

How does tightening capacity affect shippers?

As trucks get scarcer relative to freight, carriers reject more tenders and loads fall to a more expensive spot market, so shippers face firmer rates and tougher coverage. Whether or not you call the cause a driver shortage, the effect is the same. Shippers without deep carrier networks feel it first, with some seeing increases above 25% on the tightest lanes.

Is truckload capacity tightening in 2026?

Yes. Tens of thousands of carriers and drivers have exited since 2022, tender rejections have roughly doubled year over year to around 14% in early 2026, and spot rates have risen for several consecutive months. Most forecasters expect a firmer capacity market through the back half of 2026.

Will electric or autonomous trucks fix tightening capacity?

Not in the near term. Electric trucks like the Tesla Semi target operating cost and emissions, not the number of trucks or drivers available, and they still need a driver. Autonomous trucks target labor, but driver-out operations currently number in the dozens against millions of trucks on the road, with commercial autonomy expected in the single digits of long-haul lanes by the early 2030s. Both matter long-term; neither covers your freight this year.

How can shippers secure capacity in a tight market?

Widen your carrier network so more quality carriers compete for your freight, make your loads attractive with fast, flexible operations, get your spot and contract mix right and revisit it often, and use real-time market-rate data so you can adapt as lanes tighten. Network depth and visibility are what keep you covered.

The driver shortage debate will keep running. The capacity trend underneath it is clearer: fewer trucks, firmer rates, and a market that rewards shippers who prepared.

You can't control how many drivers enter the market or how fast autonomous trucks arrive. You can control how much capacity competes for your freight and how quickly you see the market move. That's what resilience looks like, and it's what keeps you covered when the market tightens.

Ready to reinvent your procurement strategy?